COVID-19 continues to disrupt consumer markets though demand is almost back to normal in most parts of India. The second edition of Bizom's COVID-19 Impact India report shares insights on the performance of the market from April to June as consumer businesses start to recover with easing of the lockdowns.

To develop the report, Bizom analysed data from approximately 30% of the retail universe across 400 districts, 2000 towns and cities of India, which covers a population of 800+ million.

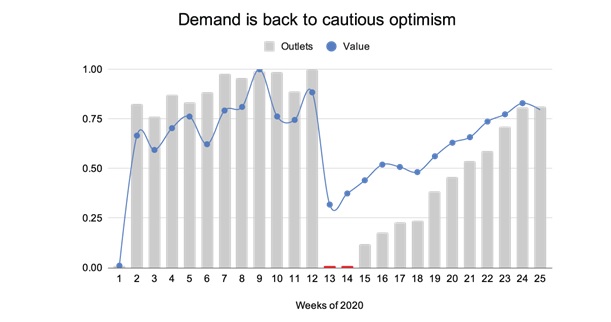

From market data of the last 10 weeks, it is clear that recovery is well and truly underway. However, a few categories - Beverages and Personal Care continue to struggle and will see a massive impact on their sales volumes. Brands are adapting to the new normal by changing their route to market models and through large scale digital transformation of their supply chains.

|

Chart 01: Week-wise breakup of demand from transacting outlets

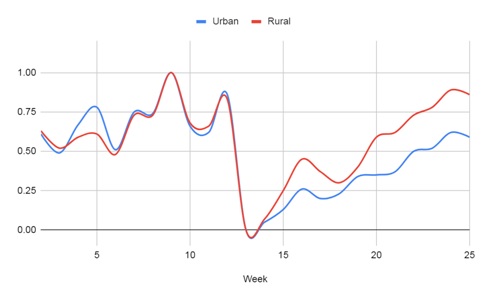

Also, rural India is recovering faster and average sales for rural was 40% higher than urban in June. Focus on rural is paramount for brands to drive growth and recover lost sales. The research involved analysing total sales data of 87 cities including metros, state capitals, B class cities etc.

|

Chart 2: Demand break up in rural vs urban areas

First among the key trends is the change in buying patterns from distributors, stockists and retailers. These channel partners are moving away from monthly and fortnightly replenishments of their stocks to weekly cycles. The trend is driven by a range of factors including stock availability and ability to give credit in the market among others.

Many brands are re-inventing trade models as they look to combat disruptions in their supply chains. They are relying on internal and external data, and investments in digital technologies to make strategic decisions that can improve their retail execution. They are beginning to rely on data insights to target stores with limited availability of their products. To enhance their customer targeting capabilities, they are using hyper-local data to identify regions and stores that are open in containment zones or are transacting even in times of lockdown. They are also signing up with tech-driven logistics partners to drive last mile order fulfilment.

To power these strategic changes, consumer brands are depending on digital technologies such as self-service apps where retailers can send their orders directly to the brand. Conversational commerce is fast gaining popularity where brands are engaging with consumers through WhatsApp and redirecting them to the nearest store that stocks the brand's products. These technological changes are aimed to make remote retail execution possible where all stakeholders in the downstream supply chain are digitised and salespeople can conduct their business on phone and through on-call solutions.

Performance across categories is almost back to normal levels though some regional and category variances exist. For example, Packaged Foods which saw a surge immediately after the first lockdown is now down by approximately 20%. However, it is Beverages that was most affected with almost 40% loss of sales at its peak season in April and May. Regionally, South India is performing better than other regions. West is lagging behind in recovery which is in line with the high incidence of COVID-19 cases in the region.

Brands are changing their RTM strategies in a bid to recover lost ground. Some of these changes include simplification of the supply chain. Sales data from April and May shows that brands are consolidating their product portfolio for operational reasons. They are focused on a smaller number of SKUs and fewer product launches. Consumers who are feeling the pinch of lowering incomes are also shifting to lower priced products or smaller pack sizes. The silver lining in the gloomy insights is that data from June shows that the industry is moving back to pre-lockdown levels and number of lines trading is now only approximately 10% as compared to February 2020.

|

Chart 3: Variation in demand for low, medium and high-value SKUs between pre-lockdown and unlock-1

A significant number of Bizom's customers across categories are investing heavily in digital technologies to improve their decision making and to bring more transparency in their supply chains. It includes digitisation of channel partners, investments in B2B E-commerce, remote retail execution and more. There are clear signs that B2B E-commerce is becoming an important channel for brands with categories of home care, confectionery, packaged goods and more.

Unsurprisingly, many brands are launching hygiene products which are completely outside their product portfolio. 5-10% consumer brands have launched new hand sanitisers and masks to support the COVID-19 demand.

Bizom's COVID-19 Impact report points to shifts in the consumption patterns but it's too early to say if these changes are here to stay.

For a detailed report, write to marketing@mobisy.com.

source http://newsvoir.com/index.php?option=com_content&view=release&rid=14204

0 Comments